Most European government bond markets continued their downward spiral during the week of May11th, 2015, led by a sell-off in US Treasury markets. New supply from the US Treasury pushed yields up (bond prices down) and aided a global downward trend. Europe is showing its sensitivity to uncertainty over when the fed will start to raise rates. This coupled with concerns that European bond markets are overvalued in light of the ECB’s QE expectations, and whether deflation concerns are over-hyped, are giving the market mixed signals.

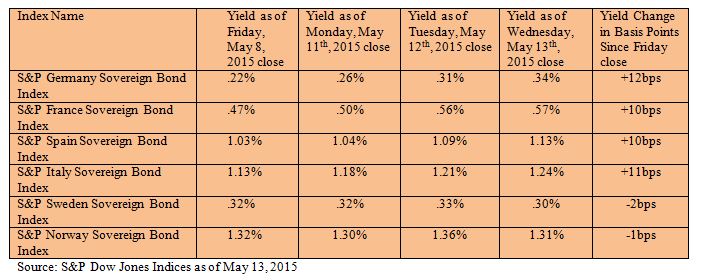

European government bond markets are moving in tandem for the most part, despite conflicting inflation numbers. While inflation is picking up in Germany and France, with consumer prices rising in both countries for the month of April YOY, Italy and Spain are seeing lower prices. Italian CPI was down at -.1% for the month of April YOY, while Spain’s CPI is at -.7% in April YOY. All four of these markets sold off causing yields to spike 10bps and up since Friday’s close.

Norway and Sweden did not sell off and actually rallied on Wednesday. Swedish consumer prices declined .2%, causing concerns that Sweden will need to lower rates further. From Friday’s close, the S&P Sweden Sovereign Bond Index yield tightened 2bps to close at .30% as of Wednesday. Norway’s CPI for April clocked in at 2% YOY, and its bond market rallied as well. The S&P Norway Sovereign Bond Index, initially sold off on Tuesday only to bounce back again along with Sweden. The S&P Norway Sovereign Bond Index tightened 1bps to 1.31% for the same timeframe.

The posts on this blog are opinions, not advice. Please read our Disclaimers.