On May 4, 2015, the Saudi Arabian Capital Market Authority (CMA) released the “Rules for Qualified Foreign Institutions Investment in Listed Shares,” or the QFI program, setting the stage for institutional investors based outside of the Gulf Cooperation Council (GCC) to make direct investments in Saudi Arabian equities for the first time. Although additional steps will need to be taken to further improve market accessibility in the future, the QFI program is a key step in the development of Saudi Arabia’s equity market.

The QFI rules, which are expected to become effective on June 1, 2015, require institutions to register with the CMA and meet certain qualifications based on assets under management and experience in the financial services industry. In aggregate, all QFIs will be allowed to own a maximum of 20% of any listed company and a single QFI will be limited to a 5% stake in a single company.

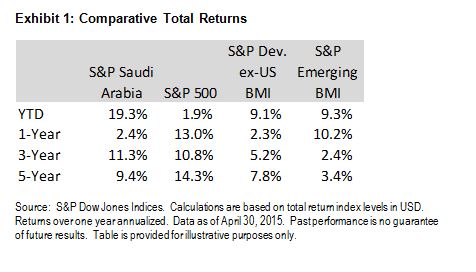

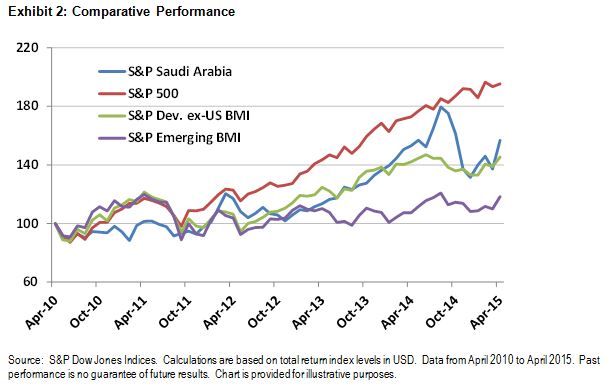

Without a doubt, the QFI program marks a historic moment for Saudi Arabia’s capital markets. Anticipation surrounding the opening of the Saudi Arabian market to foreigners has buoyed the country’s equity market over the past few years, despite a significant drop in the second half of 2014 driven by the plunge in oil prices. As of April 30, 2015, the S&P Saudi Arabia had an annualized return of 11.3% over the past three years, widely outperforming the 2.4% return of the S&P Emerging BMI and even beating the 10.8% return of the S&P 500®.

S&P Dow Jones Indices calculates and publishes more indices than any other provider for the Saudi Arabian market and throughout the GCC. Through our acquisition of the International Finance Corporation (IFC) Indices in 2000, we have been calculating Saudi Arabian equity indices since 1997.

In addition to our flagship S&P Saudi Arabia Index, we publish various size, sector, and industry subindices that are designed to measure different segments of the market. We also publish blue-chip indices, such as the Dow Jones Saudi Titans 30 Index, that are designed to support index-based financial products. We also provide multiple versions of various indices reflecting the differing opportunity sets available to domestic Saudi Arabian investors and GCC nationals due to foreign investment restrictions.

The posts on this blog are opinions, not advice. Please read our Disclaimers.