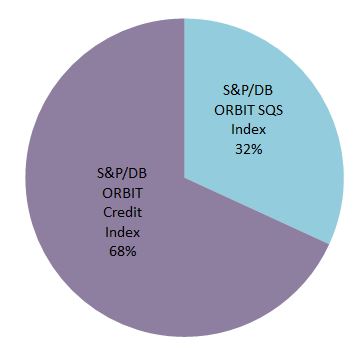

On the back of strong issuance this year, the size of the dim sum (as known as Offshore Renminbi) bond market, that tracked by the S&P/DB ORBIT Index, rose 57% year-to-date (YTD) to currently CNH 264 billion. As shown in Exhibit 1, 68% of the dim sum bond market is composed of the credit issuers. Note that the index targets to track the most liquid segment of the market, the bond must meet a minimum outstanding par of RMB 1 billion in order to be eligible to enter into the index.

Exhibit 1: The Sector Breakdown by Market Value

The credit sector contributed most to the growth in market value; the top 5 largest issuers of this year were China Unicom, China Construction Bank, China Eastern Air, Hainan Airline and Beijing Capital. While there is an increasing concentration of Chinese credits, it is good to see some foreign names and returning issuers such as Volkswagen and Caterpillar that brought in the diversity.

According to the S&P/DB ORBIT Index, the total return rose 2.03% YTD while the yield to maturity widened by 40bps to 4.07%, as of August 6, 2014. The solid gain reflected better investor sentiment, benefited from the improving economy and the stabilizing currency. As a reference, the 5-year and 10-year China Government Bond (CGB) are trading around 3.02% and 3.81%, respectively.

Despite the concern of the deteriorating credit quality early this year, the S&P/DB ORBIT Credit Index outperformed the S&P/DB ORBIT Sovereign and Quasi-Sovereign Index, which were up 2.18% and 1.76%, respectively. Please see Exhibit 2 for the total return performance.

The yield spread between the S&P/DB ORBIT Credit Index and the S&P/DB ORBIT Sovereign and Quasi-Sovereign Index surged from 120bps at the end of last year to 159bps. It seems that while the supply remains robust, the chase for yield continues to support the market.

Exhibit 2: The Total Return Performance of the S&P/DB ORBIT Index Family

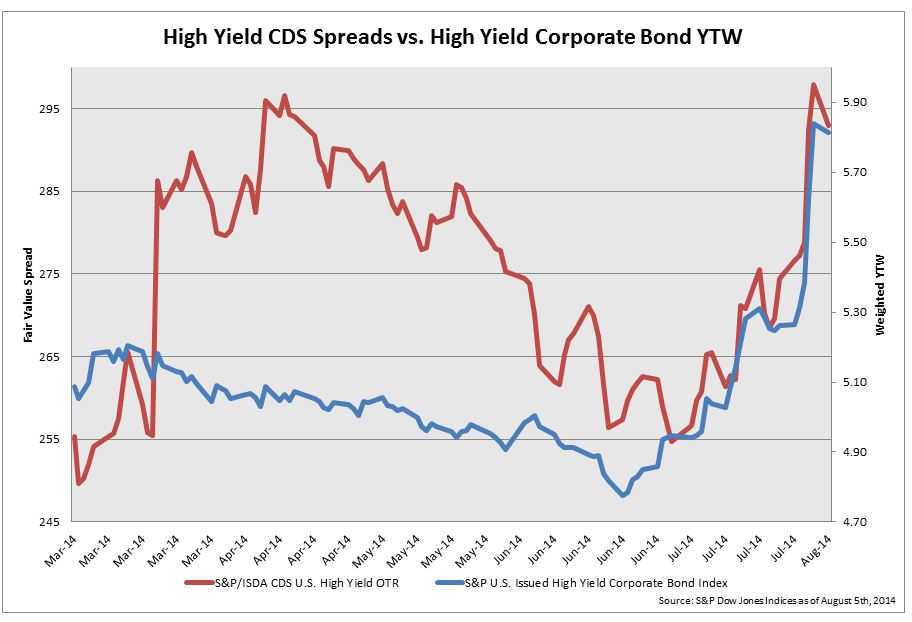

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.