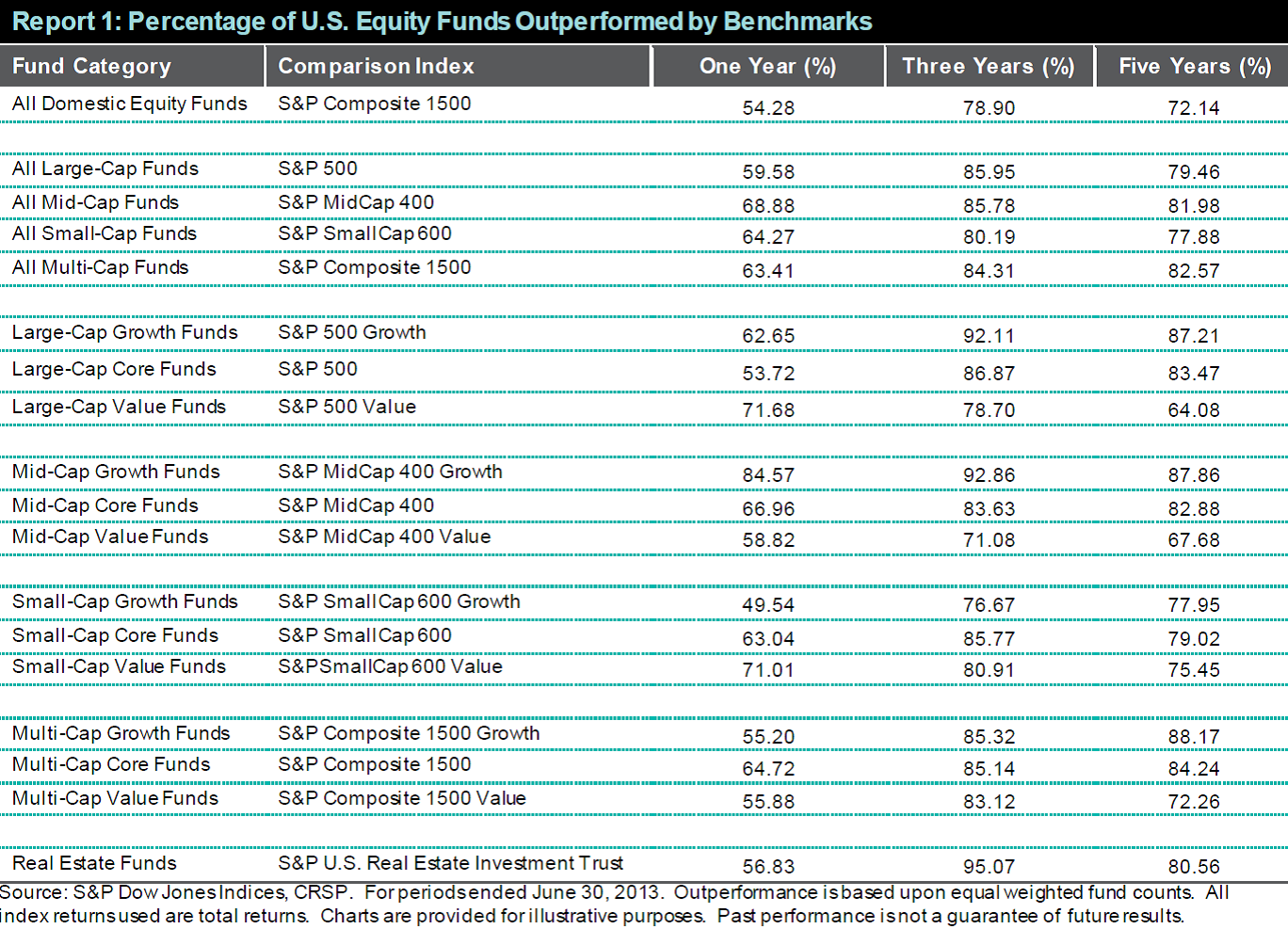

The past 12 months ending June 30 saw an impressive rally in the domestic equity markets with S&P 500, S&P MidCap 400 and S&P SmallCap 600 posting double digit gains. During that period, the majority of active managers in all the categories except small cap growth underperformed their benchmarks. The SPIVA 2013 mid-year report shows that over the past twelve months, 59.58% of large-cap funds, 68.88% of mid-cap funds and 64.27% of small-cap funds underperformed their respective benchmark indices. The figures are even more underwhelming when viewed over the three- and five- year horizons. The majority of the active managers in all the domestic equity categories underperformed their respective benchmarks.

The report also highlights another investing myth. Active investing is thought to be a better way to access less efficient markets such as small cap equity than passive investing. However, as the SPIVA Scorecard shows, 77.88% of actively managed small cap funds underperform the S&P SmallCap 600 over the past five years. If we go back further, say to the end of 2006, we can see that nothing much has changed. Over the five year period ending December 31, 2006, 76.47% of small cap managers underperformed the benchmark. This, of course, poses an interesting question of how much of the Efficient Market Hypothesis has been wrongly used to propel the myth of active investing for small cap equity.