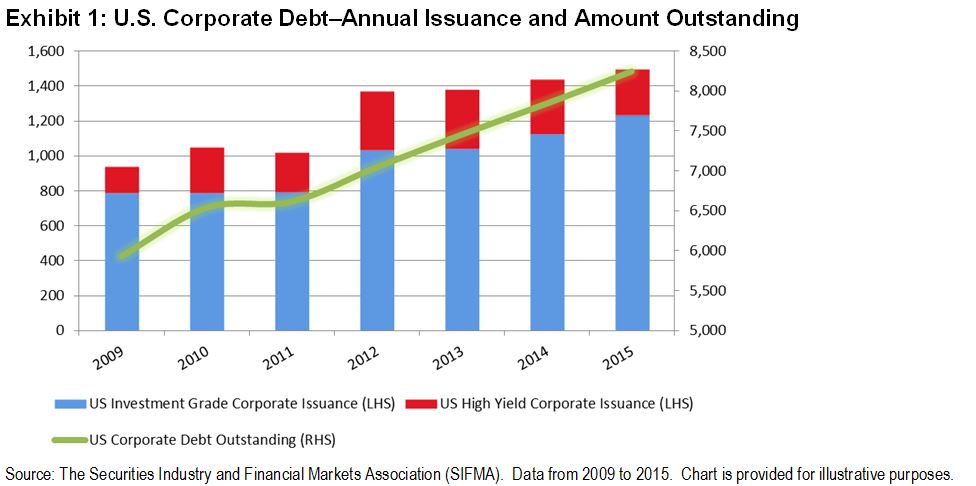

As of Feb. 26, 2015, the U.S. corporate bond market was valued at USD 8.3 trillion.[1] For comparison, that’s larger than the GDP of Germany, France, and the U.K. combined. Exhibit 1 details the growth of the U.S. corporate debt market since 2009, showing annual issuance amounts for both investment-grade and high-yield debt. Since 2012, there has been USD 1.3 trillion[2] of U.S. high-yield corporate debt issued—more than the total amount issued in the prior 10-year period (2002-2011).

Given the low interest rate environment and the increased demand for yield, many U.S. corporations have taken advantage of the opportunity to borrow at lower costs. What is interesting is how increased borrowing may not necessarily contribute to long-term growth. Rather than investing in assets or technology, many companies used the proceeds from debt issuances to pay dividends or support buyback programs. As evidence, dividends paid out by companies in the S&P 500® in 2015 amounted to the highest proportion of their earnings since 2009.

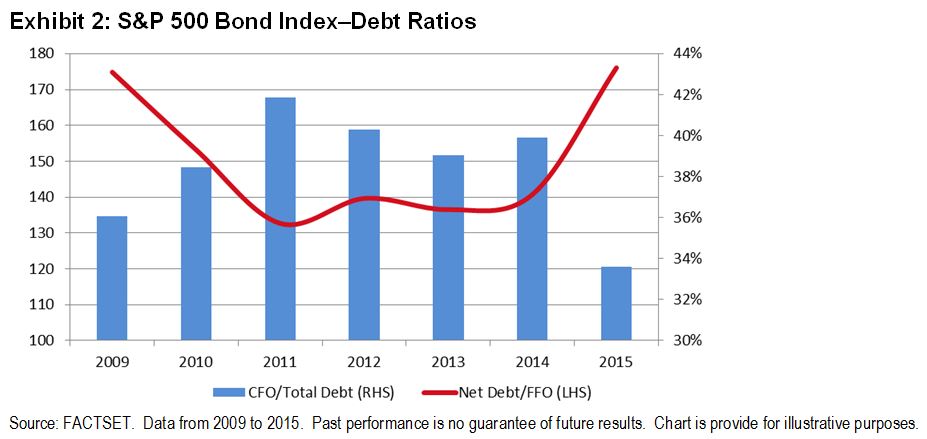

Further, using the constituents of the S&P 500 Bond Index, measures of debt relative to cash flows are at levels not seen since 2008 (see Exhibit 2).

Also noteworthy is the amount of U.S. corporate debt that is scheduled to mature in the next five years. Recent reports from rating agencies state that as much as USD 4 trillion[3] in U.S.-rated corporate debt is set to mature through 2020.

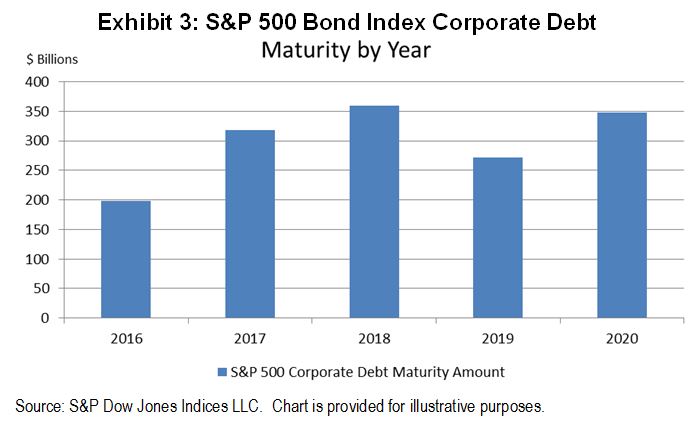

Of the USD 3.7 trillion of corporate debt tracked by the S&P 500 Bond Index, over USD 1.5 trillion (approximately 40%) is set to mature through 2020 (see Exhibit 3).

While the past six years have been conducive for corporate debt issuance, the current environment of easy monetary conditions may not continue. As seen with the recent turmoil with high-yield debt, the market’s ability or willingness to support debt refinancing is not always present. As credit concerns escalate, corporations may face the possibility of increased funding costs or limited refinancing options.

[1] Source: SIFMA

[2] Source: SIFMA

[3] Source: Standard & Poor’s Ratings Services Credit Services Ratings & Research (RatingsDirect®)

The posts on this blog are opinions, not advice. Please read our Disclaimers.