During festivals such as Diwali, the demand for gold in India increases because it is considered auspicious. Traditionally, people invested in physical gold bars, coins and jewelry. However, after the introduction of the gold ETF, the option to invest in gold also became popular. There was a huge growth in the assets under management for gold ETFs compared with ETFs in other asset classes.

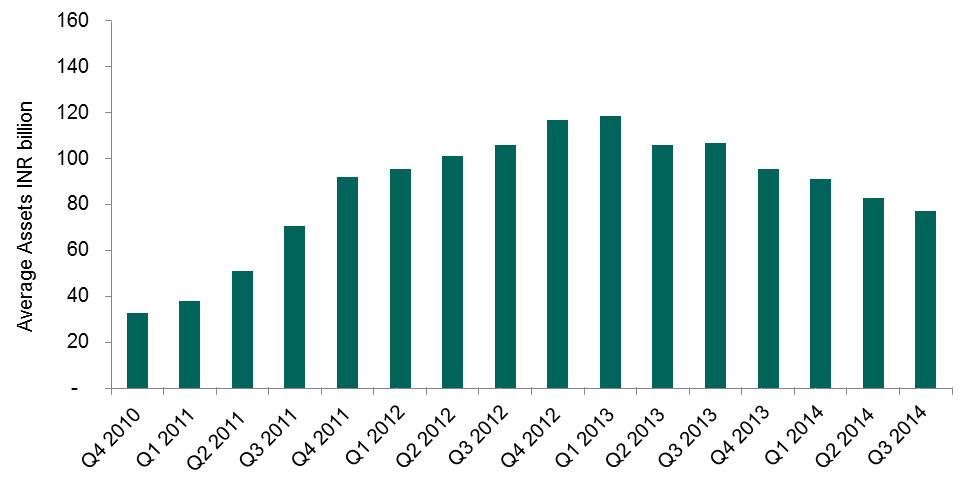

Investors purchased gold as a way to preserve value and hedge against inflation and recession. Gold was in a bull run until the year 2012, and the average asset under management in gold ETFs peaked at INR 119 billion in Q1 2013, but since then it has declined.

Exhibit 1: Average Assets in Gold ETF’s in India

Source: Association of Mutual Funds of India. Data as of Sept. 30, 2014

The Federal Reserve introduced tapering after confidence of the sustained improvement in the U.S. economy was restored. Tapering led to the strengthening of the U.S. dollar, which exerted downward pressure on the price of gold. The import restrictions in India, the second largest consumer of gold, exacerbated the situation.

The Indian government and the Reserve Bank of India introduced a series of measures in 2013 in an effort to curb the import of gold and improve the current account balance of payments of India. The introduction of the 80:20 rule, under which 20% of the imports must be re-exported, and an increase in import tariffs has reduced the amount of gold imported, and it has increased gold’s premium in the local market compared with that of the global market.

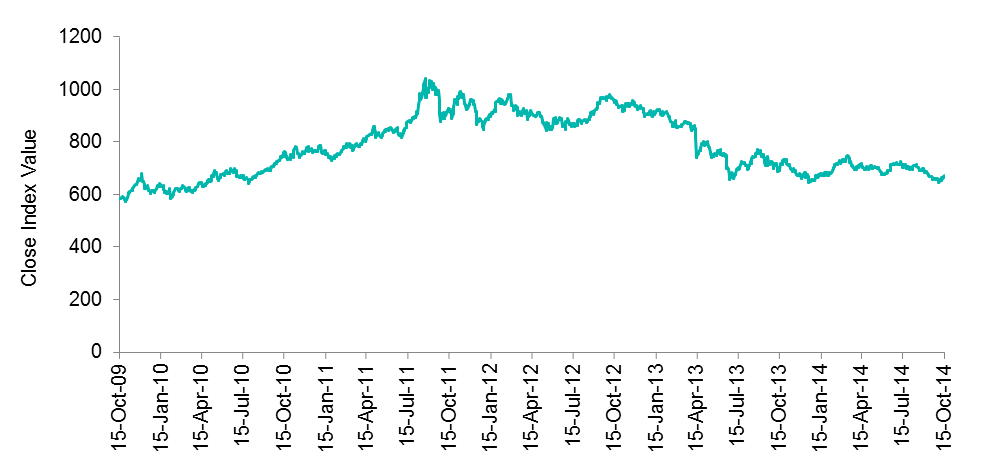

Looking at Exhibit 2, we can see that the S&P GSCI® Gold TR, which measures the returns accrued from investing in fully collateralized gold futures contracts, has been in a declining trend. It has lost nearly 8.91% and 9.78% over the one- and three-year periods ending in September 2014, respectively.

There has also been a shift in the sentiment toward investments in equity and bond markets because of higher returns. These all are included as some of the reasons for the decline in the price of gold after the 11-year bull run. However, with the ongoing economic crisis in Europe and among the emerging markets, gold may still benefit as a safe haven hedging tool.

Exhibit 2: S&P GSCI Gold TR

Source: S&P Dow Jones Indices LLC. Data as of Oct. 15, 2014. Charts and tables are presented for illustrative purposes. Past performance is no guarantee of future results.

The posts on this blog are opinions, not advice. Please read our Disclaimers.