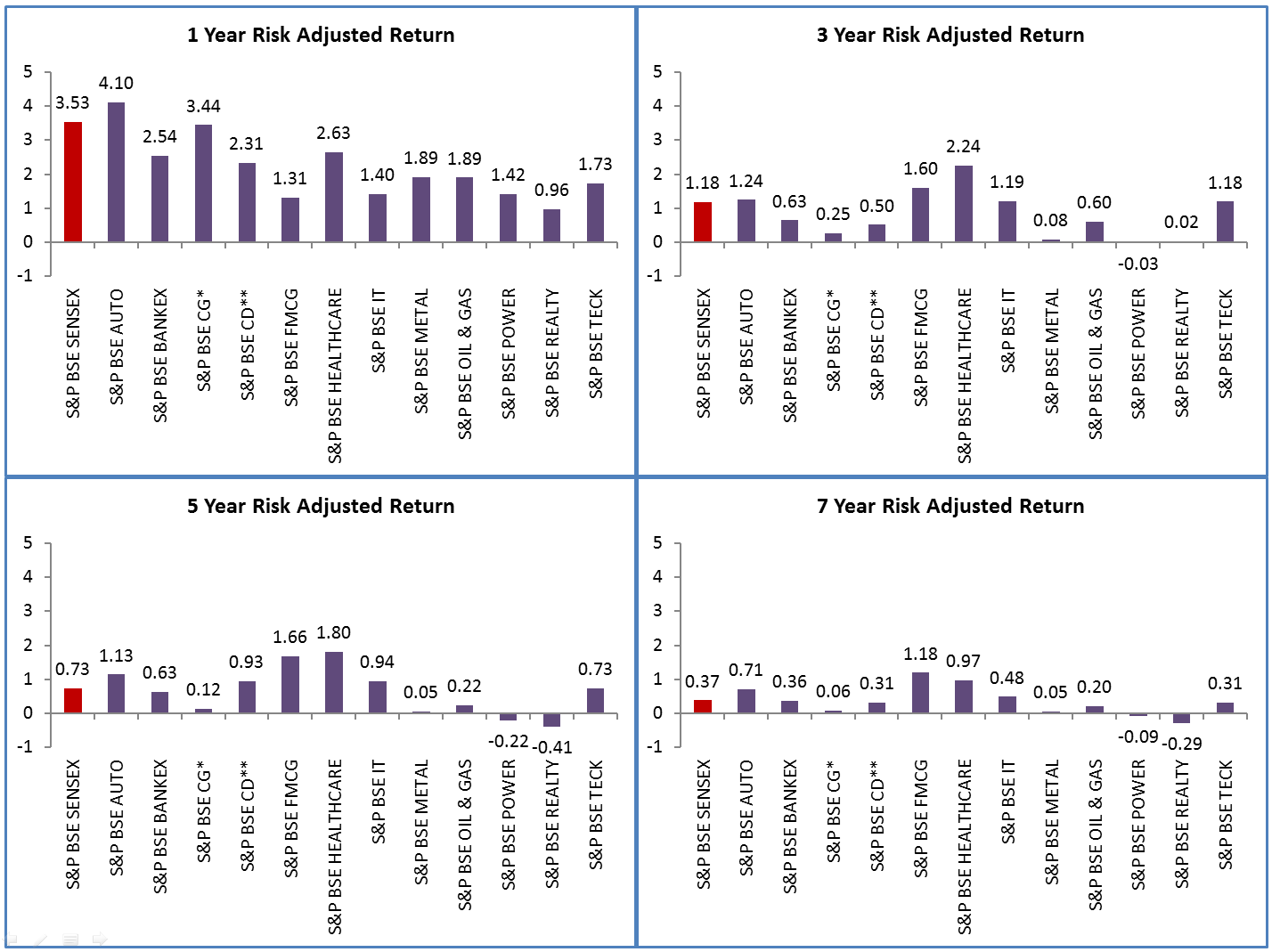

The stock markets in India have performed phenomenally in the recent months. The S&P BSE SENSEX (India’s most tracked bellwether index) has been scaling heights never seen before. The one-year, risk-adjusted return of the index was approximately 3.53 as of August 29, 2014. With 30 stocks, the index is well diversified across sectors. It will be intriguing to explore the performance of the sectors with the help of S&P BSE sector indices for the one-, three-, five- and seven-year time periods ending on August 29, 2014. All the sector indices are subsets of the S&P BSE 500, and they cover approximately 90% of the market capitalization of the respective sectors in the index, giving a good idea of each sector’s performance.

In all the observed time periods, the S&P BSE AUTO has consistently yielded higher risk-adjusted returns than the S&P BSE SENSEX.

The S&P BSE BANKEX only provided risk-adjusted returns close to those of the S&P BSE SENSEX in the seven-year time period, and it remains lower than S&P BSE SENSEX for all the time periods.

Compared with the S&P BSE SENSEX, the S&P BSE CAPITAL GOODS delivered less than 25% of risk-adjusted returns in the three-, five- and seven-year time periods, and it came close to S&P BSE SENSEX in the one-year time period.

The S&P BSE CONSUMER DURABLES provided risk-adjusted returns greater than those of the S&P BSE SENSEX only for the three-year time period.

Except for the one-year time period, the S&P BSE FMCG provided higher risk-adjusted returns than the S&P BSE SENSEX over all the other observed periods. The S&P BSE FMCG has the most stable risk-adjusted return profile.

The S&P BSE HEALTHCARE also provided higher risk-adjusted returns than the S&P BSE SENSEX for all the time periods except for the one-year period.

The S&P BSE IT provided higher risk-adjusted returns than the S&P BSE SENSEX in all the time periods except for the one-year time period as well.

In the three-, five- and seven-year time periods, the S&P BSE METAL delivered less than 15% of risk-adjusted returns compared with the S&P BSE SENSEX. The S&P BSE METAL remains lower than S&P BSE SENSEX for all the time periods.

Compared with the S&P BSE SENSEX, the S&P BSE OIL & GAS has given less than 55% of risk-adjusted returns in all the time periods.

The S&P BSE POWER has been hit the hardest with negative risk-adjusted returns in the three-, five- and seven-year time periods, and it remains lower than S&P BSE SENSEX for all the time periods.

The S&P BSE REALTY has also had negative risk-adjusted returns in the five- and seven-year time periods, and it remains lower than the S&P BSE SENSEX for all the time periods.

For all except the one-year time period, the S&P BSE TECK has had a risk-adjusted return profile close to that of the S&P BSE SENSEX. The S&P BSE TECK returned almost half of the S&P BSE SENSEX in the one-year time period.

*S&P BSE CAPITAL GOODS; **S&P BSE CONSUMER DURABLES

Source: Asia Index Pvt. Ltd. Data as of last trading date of August 2014. Risk adjusted return has been calculated for total return indices. This chart may reflect hypothetical historical data. Please see the Performance Disclosures for information regarding the inherent limitations associated with back tested data. Past performance is no guarantee of future results.

The posts on this blog are opinions, not advice. Please read our Disclaimers.