Three of the Five Cities Saw Default Rates Descend in February 2013

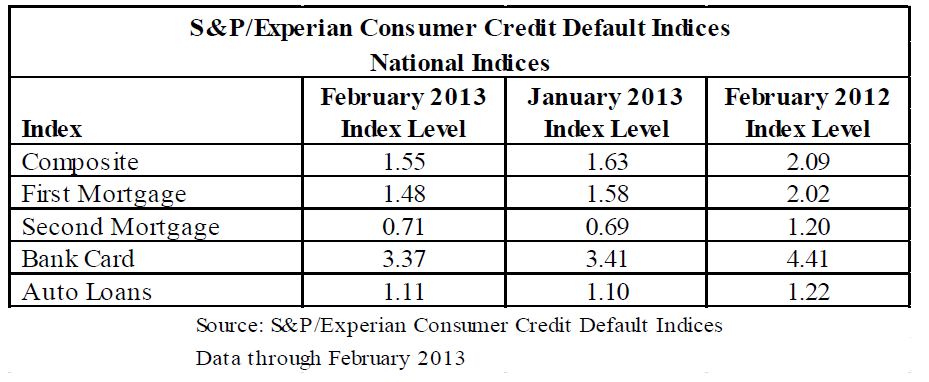

New York, March 19, 2013 – Data through February 2013, released today by S&P Dow Jones Indices and Experian for the S&P/Experian Consumer Credit Default Indices, a comprehensive measure of changes in consumer credit defaults, showed a decrease in national default rates during the month. The national composite was 1.55% in February, down from 1.63% in January.

The first mortgage default rate moved down to 1.48% in February, from 1.58% in January. The bank card rate was 3.37% in February vs. 3.41% in January. The second mortgage and auto loan default rates increased in February posting 0.71% and 1.11%; they were marginally up from their respective 0.69% and 1.10% January levels.

“Consumer credit quality remains healthy”, says David M. Blitzer, Managing Director and Chairman of the Index Committee for S&P Dow Jones Indices. “The first mortgage and bank card default rates moved down, the second mortgage and auto loans were marginally up in February. All loan types remain below their respective levels a year ago.

“These trends are consistent with other economic news – improvements in employment and overall economic activity and continuing gains in housing. Additionally, foreclosure activity continues to decline even though it remains at elevated levels compared to the period before the financial crisis.

“Three of the five cities we cover showed decreases in their default rates in February – New York was down by 12 basis points, Los Angeles by 18 and Miami by 24 basis points. Chicago was marginally up by one basis point and Dallas was up by seven basis points. Miami had the highest default rate at 3.21% and Dallas – the lowest at 1.26% among the five cities. All five cities remain below default rates they posted a year ago, in February 2012.”

The table below summarizes the February 2013 results for the S&P/Experian Credit Default Indices. These data are not seasonally adjusted and are not subject to revision.

The posts on this blog are opinions, not advice. Please read our Disclaimers.