Fifty years ago, there were no index funds—all assets were managed actively. The subsequent shift of assets from active to passive management in the U.S. and European markets could be considered one of the most important developments in modern financial history, and this shift was the consequence of active performance shortfalls.[1] In India, we have seen similar shortfalls, coupled with unique local factors that have contributed to the rapid growth of passive investments in the Indian mutual fund industry.

Cost

Lower cost has been the simplest explanation for the success of passive management. Active managers’ costs—for research, trading, management fees, etc.—have tended to be inherently higher than those of passive managers.[2] By investing via the passive route, investors can potentially save 100 bps in management fees.[3]

Increased Regulatory Oversight, Government Initiatives, and Evolving Market Microstructure

The Securities and Exchange Board of India (SEBI) introduced style and size definitions and mandated that mutual funds only manage one product offering in each style category,[4] aiming to bring standardization across the industry. SEBI also required equity fund managers to benchmark performances against total return indices (TRI).[5] Some of the other milestones include investment by the Employees’ Provident Fund Organization (EPFO) into large-cap ETFs[6] and divestment by the Department of Investment and Public Asset Management (DIPAM) since 2013, which helped to raise approximately INR 340 billion via multiple tranches among different ETFs.[7]

Real-World Returns Are Positively Skewed

The skewness of stock returns is often an underappreciated element in the performance difficulties of active managers. The intuition is simple: a manager’s picks are more likely to underperform than to outperform simply because there are more underperformers than outperformers from which to choose.[8] Active managers in India, like their U.S. counterparts, are challenged by a positively skewed equity market.

Growth of the Domestic Mutual Fund Industry

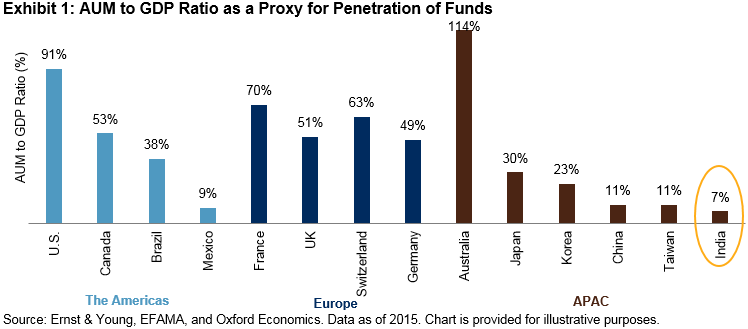

AUM/GDP is a commonly used ratio to track the penetration of mutual funds in an economy. Exhibit 1 illustrates that India (7%) has a long way to go before it reaches the stature and depth of the U.S. (91%) market. As the Indian economy matures and financial literacy improves, one could anticipate higher adoption rates of mutual fund products as a long-term savings tool. This has the potential to expand the overall size of the mutual fund industry and simultaneously raise passive investment shares.

In the U.S., the passive share of the equity mutual fund and ETF assets was approximately 45% as of the end of 2017, more than double its 20% level at the beginning of 2007.[9] In contrast, India’s share was just 3.8% as of March 2018.[10] Although India’s passive share is small, India is beginning to consider the benefits of passive investing, similar to the U.S. market during the 1970s. The Indian passive market has the potential to mirror the growth seen in the U.S., as Indian investors take note of the benefits from lessons in passive investing in developed markets and start to enable wealth creation through transparent, systematic, style-consistent, and low-cost, index-linked products.

[1] Ganti, Anu R. and Craig J. Lazzara, “Shooting the Messenger,” S&P Dow Jones Indices, December 2017.

[2] Sharpe, William F., “The Arithmetic of Active Management,” The Financial Analysts’ Journal, Vol. 47, No. 1, January/February 1991, pp. 7-9.

[3] Ganti, Anu R. and Jain, Akash, “A Glimpse of the Future: India’s Potential in Passive Investing,” S&P Dow Jones Indices, November 2018.

[4] Categorization and Rationalization of Mutual Fund Schemes, SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2017/114, Oct. 6, 2017.

[5] Benchmarking of Scheme’s performance to Total Return Index, SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2018/04, Jan. 4, 2018.

[6] “EPFO invested nearly Rs 50K cr in ETFs till June 30: Govt,” The Times of India, July 18, 2018.

[7] Recent Disinvestment, Department of Investment and Public Asset Management, Financial Year 2018-19.

[8] The challenge for stock pickers is exacerbated when the outperformers include the largest stocks in the index. See Chan, Fei Mei and Craig J. Lazzara, “Degrees of Difficulty: Indications of Active Success,” S&P Dow Jones Indices, May 2018, pp. 8-9.

[9] Whyte, Amy, “Passive Investing Rises Still Higher, Morningstar Says,” Institutional Investor, May 21, 2018.

[10] “Digital evolution,” CRISIL, August 2018. The 4% passive share is approximately 90% in equity ETFs, with the remainder in index funds and gold, liquid, and debt ETFs.

The posts on this blog are opinions, not advice. Please read our Disclaimers.