Two weeks ago inflation fears sparked by a surprise jump in wage gains sent the markets into a tail spin. This week will deliver two rounds of inflation news with the Consumer Price Index (CPI) on Wednesday and the Producer Price Index (PPI) on Thursday. Month to month changes in both the CPI and PPI are usually quite small; large moves often reverse in subsequent months. Moreover, measures of expected inflation don’t suggest a great deal of anxiety about rising prices. Nevertheless, the recent market volatility will focus a lot of attention on this week’s inflation numbers.

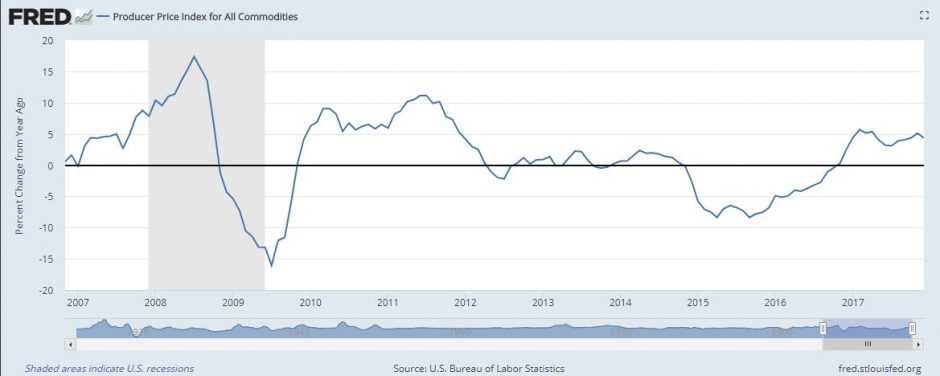

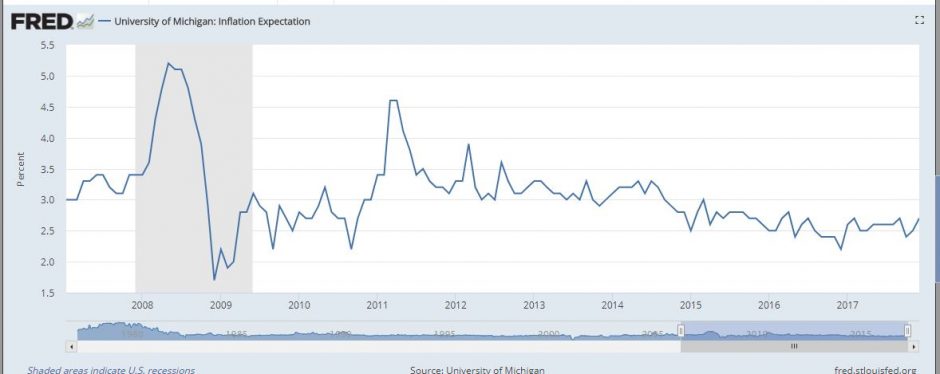

The charts shown here provide some perspective on inflation. The charts show the year-over-year change in various inflation measures as well as measures of expected inflation based on the University of Michigan Survey Research Center and the yields on five-year treasuries and TIPS.

The CPI (second chart) and PPI (third chart) do show an upward trend in inflation since 2015. This reflects rising oil prices in 2016-17 as well as an improving economy. But in both series increases in inflation appear to reverse.

Based on current surveys, the year-over-year increases in the CPI are likely to remain under 2%, the year-over-year increase in the PPI could top 2%. All these are similar to recent numbers.

The Core CPI excludes the volatile food and energy components from the CPI to give a better long term view of inflation

Even the overall CPI, including all components, doesn’t show any hints of a surging prices any time soon.

While the PPI is more volatile, it is not signaling any immediate problems.

Research and comments by various Federal Reserve officials point to expectations of future inflation as a principal determinant of future inflation. This chart shows that expectations have been stable over the last several months.

Finally, the future inflation rate implied by five year treasury notes and the inflation-protected treasury securities do hint that five years down the road, inflation will still be close to 2%.

All charts use data from FRED economic data, St. Louis Federal Reserve Bank.

The posts on this blog are opinions, not advice. Please read our Disclaimers.