Factor-based strategies have been regularly used by market participants in their portfolio construction process. Apart from the established factors like value, size, volatility, etc., research on alternative factors has remained important to explain sources of alpha. One such alternative factor is consensus analysts’ earnings forecasts. Ample empirical research exists that explains the market’s reaction to analysts’ earnings forecasts. Most of the research focuses on the change in the consensus estimate or the number of upgrades or downgrades in the estimates over short-term periods.

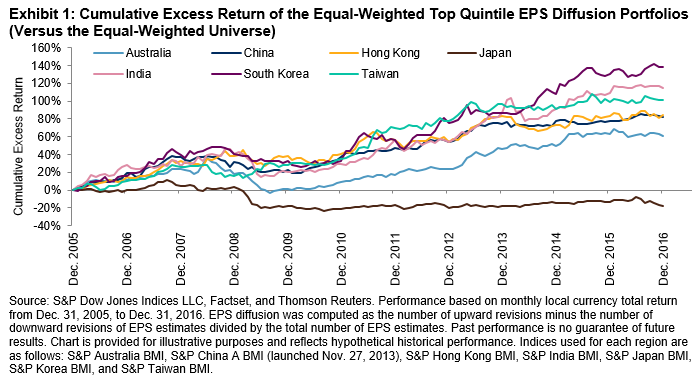

Compared with the U.S. and the European markets, the Asian market is more distributed and each individual market in Asia has its own characteristics. In our research paper Do Earnings Revisions Matter in Asia, we tested earnings revision strategies across seven Pan Asian markets—Australia, China, Hong Kong, India, Japan, South Korea, and Taiwan. We examined the three-month change in the consensus estimate and the three-month diffusion of analysts’ earnings forecasts from Dec. 31, 2005, to Dec. 31, 2016.

The key findings were as follows.

- Stock prices tended to move in the same direction as their earnings revisions in the majority of Pan Asian markets. Earnings revision strategies delivered the most significant excess returns in South Korea, India, and Taiwan, but they did not work in Japan (see Exhibit 1).

- Market participants generally had stronger reactions to the net percentage of upward and downward revisions in earnings estimates rather than the percentage change of the consensus estimate figures.

- Companies with poor earnings revisions tended to have more volatile returns, as market participants reacted negatively to companies with downward revisions in estimates.

- Earnings revision strategies tended to generate more alpha in the small-cap universe than in the large-mid-cap universe, although there was no strong sector or size bias.

Like other momentum strategies, the earnings revision strategies also had high turnover. In addition, the market-cap effect disrupted the signal from the earnings revision strategies. Therefore, implementing this strategy in combination with other fundamental factors and alternative weighting schemes would be essential to capture alpha. To find out more, please see the full report.