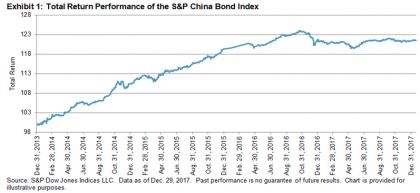

In a previous piece, we discussed that China’s lackluster performance had made it the worst-performing country in the Pan Asian bond market in 2017, and that it was the only country that closed the year in negative territory. The one-year total return of the S&P China Bond Index fell 0.29% last year (see Exhibit 1), contrasting with the strong gains observed in previous years.

The S&P China Bond Index also underperformed the broad market. The S&P Global Developed Aggregate Ex-Collateralized Bond Index (USD), which seeks to track the performance of investment-grade debt issued by sovereign, quasi-sovereign, foreign government, and corporate entities in developed countries, delivered a total return of 7.64% in 2017.

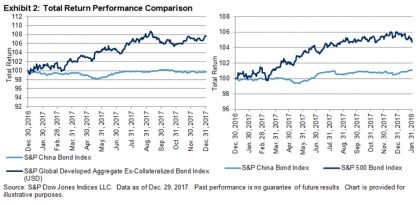

Specifically for the corporate bond sector, China lagged its U.S. counterpart. The S&P 500® Bond Index is designed to measure the performance of U.S. corporate bonds issued by the constituents of the iconic S&P 500, and it rose 6.05% last year, compared with the 0.58% gain in the S&P China Corporate Bond Index (see Exhibit 2).

In terms of yield performance, the yield-to-worst of the S&P China Bond Index widened 178 bps to 4.78%, as of Dec. 29, 2017. As a comparison, the yield-to-maturity of the S&P Global Developed Aggregate Ex-Collateralized Bond Index (USD) and the S&P 500 Bond Index were 1.41% and 3.28%, respectively.

Despite their performance, China’s solid economic growth, attractive bond yields, and the underparticipation of foreign investors may serve as positive drivers for the Chinese bond market.