In November, mid-caps led the U.S. equity market with the S&P 400 gaining 3.68%, followed by small-caps in the S&P 600 that gained 3.52% and large-caps in the S&P 500 that gained 3.07%. The S&P 500 logged its 13th consecutive positive month, the longest streak in its monthly history ever (data going back to Oct. 1989.) All eleven sectors of the S&P 500 were positive, an event that has happened just 13.9% of the time. Perhaps what is more interesting is that nine of the eleven sectors were positive together across the market caps. The last time this many sectors gained together in a month across all the market caps was in March 2016. In total, nine or more sectors have gained together across the S&P 400, S&P 500 and S&P 600 in 19.6% of months in history (since Jan. 1995.) Consumer Discretionary led both mid (+6.59%) and small caps (+7.53%) in November, making up 11.9% of the S&P MidCap 400 and 15.4% of the S&P SmallCap 600. For large caps, Telecommunication Services was the best performer, gaining 6.03%, but is the smallest sector comprising just 2% of the S&P 500.

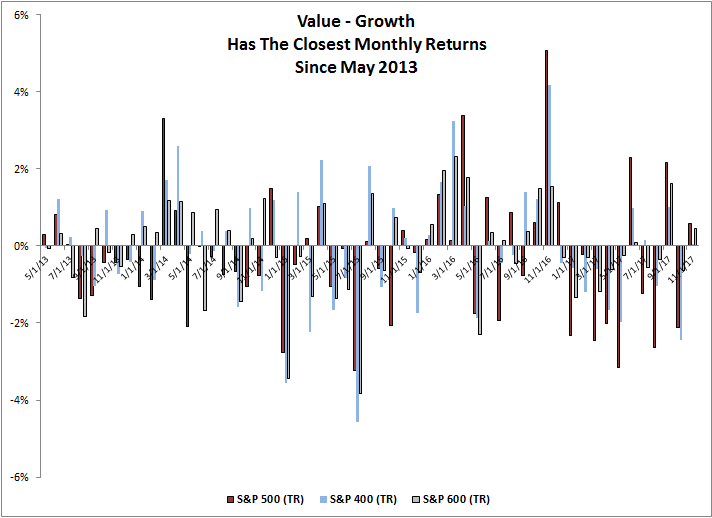

In November, the size mattered least for the value and growth styles since May 2013. The difference between value and growth for the S&P 500, S&P 400 and S&P 600 was 0.58%, 0.06% and 0.45%, respectively. In only four months in history (May 2013, July 2010, Aug. 2005 and May 2004) was the spread so tight between value and growth in mid-caps. Large caps had just a 22 basis point discount in Feb. 2017 while small caps had a tight discount of 35 basis points in Aug. 2017. In fact small caps styles have been performing very tightly in 2017, the closest since 2013 and at levels that only come this tight on a monthly basis on average per year 1/3 of the time.

That said, for the year through November in 2017, the S&P 500 Growth is outperforming the S&P 500 Value by 13.24%, the second most in history with a bigger value to growth discount only year-to-date through Nov. in 1998.

Lastly, 2017 may not be on pace to set any sector records, but for small caps, the S&P 600 Utilities and S&P 600 Health Care are having exceptionally strong performance, up a respective 26.42% and 21.48% YTD through November, on pace for their second and third best years in history. On the flip side the S&P 400 Telecommunication Services and S&P 400 Energy are on pace for their second and fourth worst years in history, down 42.55% and 21.27% for the year through November, respectively.

The posts on this blog are opinions, not advice. Please read our Disclaimers.