Common risk measures in equities include the volatility of price return and beta measuring price sensitivity to market. However, in fixed income, volatility measures for bonds are not as straightforward as equities. First, it can be challenging to obtain reliable daily prices for bonds that do not trade every day. Second, using the simple measure of price return volatility to construct a low volatility bond portfolio could introduce unintended bias. For example, given that the price return of a bond is determined by the bond’s duration and yield change, a bond portfolio constructed using the volatility measure of standard deviation of price return could be biased toward bonds with short duration.

In the construction of the S&P U.S. High Yield Low Volatility Corporate Bond Index, an individual bond’s credit risk in a portfolio context is measured by its marginal contribution to risk (MCR), calculated as the product of its spread duration and the difference between the bond’s option adjusted spread (OAS) and the spread-duration-adjusted portfolio average OAS (see Equation 1). This definition allows for measuring the incremental contribution of each bond to the portfolio credit risk within the framework of duration times spread (DTS).

![]()

DTS is an industry-accepted measure of credit risk for corporate bonds, and is calculated by multiplying spread duration and OAS (see Equation 2). Similar to spread duration capturing bond price sensitivity to spread change, DTS measures bond price sensitivity to the percentage change of OAS (Equation 3). Ben Dor, Dynkin, Hyman, Houweling, Leeuwen, and Penninga (2007) demonstrate that spread changes are proportional to the level of spreads, i.e., the volatility of percentage spread change is much more stable than absolute spread volatility, and therefore they propose that the better measure of exposure to credit risk is not the contribution to spread duration, but the contribution to DTS.

MCR borrows the concept of DTS by multiplying spread duration by the difference between bond OAS and portfolio average OAS, instead of OAS directly. By doing so, bonds with low MCR will include those with long spread duration and below average OAS, as well as those with short spread duration and above average OAS. By selecting bonds with low MCR, the low volatility index keeps more credit exposure (long spread duration) for high-quality bonds (low OAS) and less credit exposure (short spread duration) for low-quality bonds (high OAS). Overall, this reduces the spread duration mismatch between the low volatility index and the underlying universe. In the case of stressed bonds with extremely short spread duration, ranking MCR instead of DTS makes it less likely to rank stressed bonds in the lower end, and therefore reduces the likelihood of classifying stressed bonds as low volatility.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

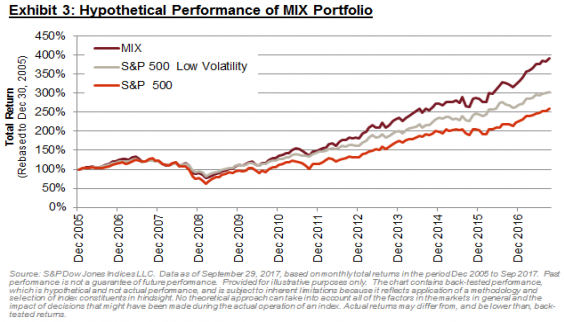

On a hypothetical basis, the MIX portfolio achieved roughly 100% upside capture (i.e. it did not lag in bull markets), while retaining a considerable degree of protection (77% downside capture). The MIX portfolio also demonstrated favourable performance statistics over longer periods. Over all possible rolling 12-month periods during our study, Low Volatility outperformed around 59% of the time; this increases to 72% for the MIX portfolio (Exhibit 5).

On a hypothetical basis, the MIX portfolio achieved roughly 100% upside capture (i.e. it did not lag in bull markets), while retaining a considerable degree of protection (77% downside capture). The MIX portfolio also demonstrated favourable performance statistics over longer periods. Over all possible rolling 12-month periods during our study, Low Volatility outperformed around 59% of the time; this increases to 72% for the MIX portfolio (Exhibit 5). The

The