Despite today’s very low inflation the Fed keeps raising interest rates and is now discussing when to shrink its balance sheet to further tighten monetary policy. The Fed’s own inflation forecast anticipates continued low inflation at 1.6% in 2017 creeping up to 2% in 2018 and 2019 and not seeing any increase later on. Moreover, consumers and the public have similar expectations for low inflation now and in the future. So why is the central bank pushing interest rates higher?

The principal reason is the belief that a low and falling unemployment rate is a reliable signal of future inflation. This is part of the received wisdom of economic policy which has some basis in the data. It originated with work done by a New Zealand economist, A. W. Phillips, in 1958 comparing unemployment and changes in wages in Great Britain from 1861 to 1957. Phillips found a consistent relation that showed lower unemployment rates were associated with higher rates of wage inflation. While the original finding was empirical – based on the data rather than economic theory – the idea soon became the basis for various theories of what causes inflation and how economic policy could lower either inflation or unemployment.

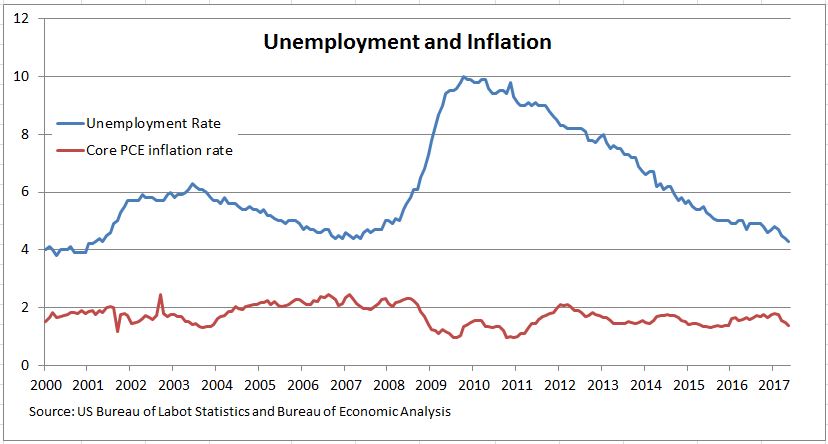

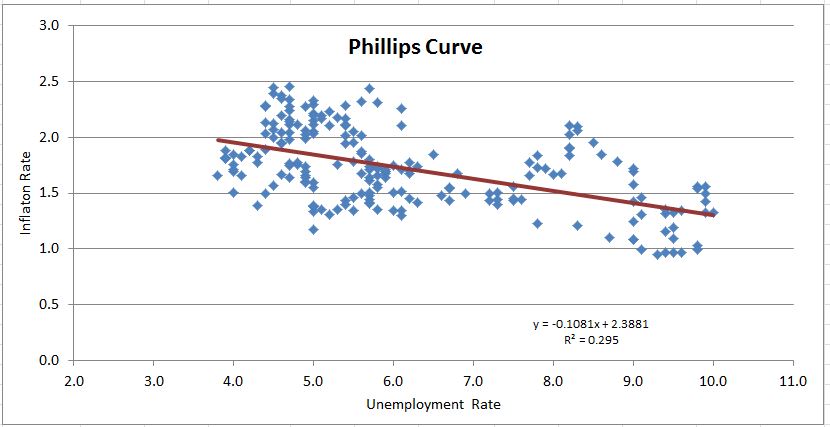

Current data on the U.S. economy since 2000 reveals similar patterns. The first chart shows the unemployment rate and the inflation rate (measured as the year-over-year change in the Core Personal Consumption Expenditures deflator) from January 2000 to May 2017. As shown, when unemployment rose in 2008, inflation fell, suggesting an inverse relation. The second figure is the Phillips curve of inflation and unemployment. It plots the unemployment rate on the horizontal axis and the inflation rate on the vertical axis. The regression line indicates that a one percentage point increase in unemployment is associated with a one-tenth of one percentage point decline in inflation.

The Phillips curve doesn’t prove that falling unemployment causes higher inflation. However the idea of a trade-off between inflation and unemployment is embedded in a lot of economic thought. Economists who remember the high inflation of the 1970s and the pain of the 1980 and 1981-2 recessions when unemployment surged and inflation collapsed pay attention to the Phillips curve. The experience of the last 12 months when both inflation and unemployment fell together isn’t enough to erase the Phillips curve.

Based on a combination of experience, data and economic theory, the Fed believes that continued declines in unemployment point to higher inflation rates. At some point the unemployment rate will hit bottom, inflation will be driven higher and a series of rapid increases in interest rates will be necessary. The result of that move could be a recession.

A related argument for gradual increases in interest rates is to prepare for the next recession: Were the economy to contract and the unemployment rate to rise, the Fed would want to lower interest rates. With the fed funds rate at 1.0%-1.25% and ten year treasuries trading at 2.4%, there isn’t much room to cut. If the Fed slowly pushes interest rates back to more normal levels with the Fed Funds rate at 3%, its ability to stimulate the economy during a recession would be improved.

The posts on this blog are opinions, not advice. Please read our Disclaimers.