Those who invest in active funds may expect portfolio managers to deliver excess returns over their benchmark indices for the fee they paid. However, results from the SPIVA® (S&P Indices Versus Active) India Scorecard suggest this may not always be the case. The scorecard, which is a biannual report, attempts to capture the performance of active funds (both equity and debt funds) domiciled in India against S&P BSE benchmarks over different time horizons.

In our extended study of Indian Equity Large-Cap and Indian Equity Mid-/Small-Cap fund performance, we found that fund managers did not deliver persistent outperformance across market cycles. We divided the ten-year period ending December 2016 into three market regimes, including bear (peak to trough), recovery (first 12 months after the trough), and bull phase (from recovery to the peak), based on the S&P BSE Sensex total return performance, and examined performance of the Indian Equity Large-Cap and Indian Equity Mid-/Small-Cap funds in different markets (see Exhibit 1). We also compared asset-weighted and equal-weighted excess returns versus the benchmarks for these two categories, in order to understand how the larger funds (by assets under management) performed against their peers.

| Exhibit 1: Illustrative Market Cycles | |

| MARKET CYCLE PHASE | PERIOD |

| Bear Market Periods | December 2007-February 2009 |

| December 2010-December 2011 | |

| February 2015-February 2016 | |

| Bull Market Periods | December 2006-December 2007 |

| February 2010-December 2010 | |

| December 2012-February 2015 | |

| Recovery Periods | February 2009-February 2010 |

| December 2011-December 2012 | |

| February 2016-December 2016 | |

Source: S&P Dow Jones Indices LLC. Data from December 2006 to December 2016. Table is provided for illustrative purposes.

We observed that the fund returns in these two categories had relatively low beta across different market cycles, which may have been driven by allocation to cash or defensive/low beta stocks in their portfolios. As a result, the active funds tended to outperform by a more significant margin in bear markets and by a relatively modest margin in bull markets. This also indicates that the alpha generation by fund managers’ stock selection was more limited during bull markets, which may not be expected.

| Exhibit 2: Beta and Active Fund Average Excess Return in Bull, Bear, and Recovery Markets | ||

| MARKET CYCLE | INDIAN EQUITY LARGE-CAP | INDIAN EQUITY MID-/SMALL-CAP |

| BETA | ||

| Bull | 0.95 | 0.84 |

| Bear | 0.89 | 0.82 |

| Recovery | 0.89 | 0.79 |

| EXCESS RETURNS VERSUS BENCHMARK (EQUAL-WEIGHTED, ANNUALIZED, %) | ||

| Bull | 0.0 | 2.0 |

| Bear | 0.4 | 6.7 |

| Recovery | -3.0 | -6.3 |

| EXCESS RETURNS VERSUS BENCHMARK (ASSET-WEIGHTED, ANNUALIZED, %) | ||

| Bull | -0.2 | 2.3 |

| Bear | 0.8 | 8.4 |

| Recovery | -1.6 | -5.9 |

Source: S&P Dow Jones Indices LLC. Benchmark for Indian Equity Large Cap is S&P BSE 100 and for Indian Equity Mid/Small Cap is S&P BSE MidCap. Beta calculated using Asset-Weighted Fund Returns. Data from December 2006, to December 2016 based on SPIVA India Year-End 2016 Scorecard. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

Furthermore, active funds outperformed in trend-continuation markets and underperformed when the market regime changed, as active funds underperformed their benchmark indices by large margins and their return betas versus their benchmark remained low during recovery phases. This implied that most fund managers may not have reduced their cash positions or tilted their portfolios to less defensive stocks when the market recovered from market downturns.

Indian Equity Large-Cap and Indian Equity Mid-/Small-Cap funds did not deliver persistent outperformance across different markets; they underperformed or had limited outperformance versus their benchmark for the 10-year period, as reported in our latest SPIVA India Scorecard. It is also clear that larger funds in these two categories tended to perform better than smaller funds across different market cycles.

To discover more about the performance of Indian active funds versus their benchmarks, check out the SPIVA India Year-End 2016 Scorecard.

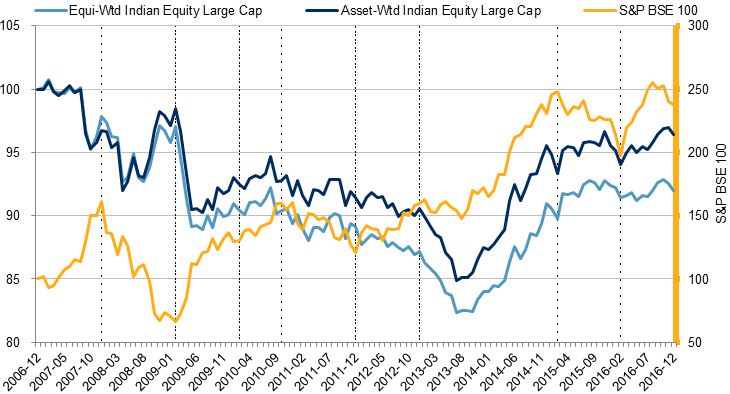

Exhibit 3: Outperformance of Indian Large-Cap Funds Versus the S&P BSE 100

Source: S&P Dow Jones Indices LLC. Data from December 2006 to December 2016 based on SPIVA India Year-End 2016 Scorecard. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

Source: S&P Dow Jones Indices LLC. Data from December 2006 to December 2016 based on SPIVA India Year-End 2016 Scorecard. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

Exhibit 4: Outperformance of Indian Mid-/Small-Cap Funds Versus the S&P BSE Midcap

Source: S&P Dow Jones Indices LLC. Data from December 2006, to December 2016 based on SPIVA India Year-End 2016 Scorecard. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE Midcap was launched on April 15, 2015.

Source: S&P Dow Jones Indices LLC. Data from December 2006, to December 2016 based on SPIVA India Year-End 2016 Scorecard. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE Midcap was launched on April 15, 2015.