Global currency sukuk continued to expand in 2016. Increasing issuances were observed in U.S. dollar, Indonesian rupiah, and Pakistani rupee sukuk, though there were decreases in Malaysian ringgit and Bangladesh taka sukuk compared with last year.[1] The U.S. dollar and Malaysian ringgit sukuk continued to dominate the sukuk market.

The Dow Jones Sukuk Index, which seeks to track U.S. dollar-denominated, investment-grade sukuk, added 17 new sukuk with a total par amount of USD 13.5 billion into the index. Sovereign sukuk continued to dominate the issuance, including USD 2.5 billion from Indonesia, USD 1.5 billion from Malaysia, USD 1 billion from Turkey, and USD 500 million from Oman. The biggest corporate sukuk issuances were USD 1.5 billion from IDB Trust, USD 1.2 billion from DP World, and USD 1 billion from Emirates Islamic Bank. Among all the new issuances, 33% was from the United Arab Emirates.

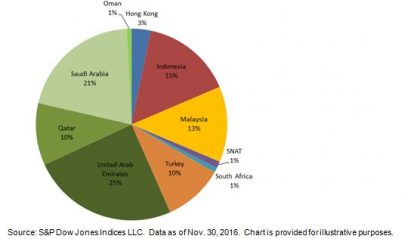

Looking at the overall country issuance in the Dow Jones Sukuk Index in Exhibit 1, Gulf Cooperation Countries (GCC) remained the largest contributor, at 57%. For the non-GCC countries, the three biggest are Indonesia, at 15%, Malaysia, at 13%, and Turkey, at 10%.

Exhibit 1: Countries of Risk of the Dow Jones Sukuk Index

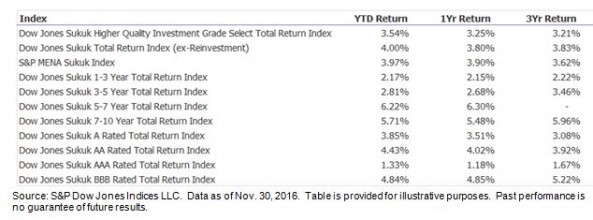

In terms of total return performance, the Dow Jones Sukuk Index rose 4.00% YTD as of Nov. 30, 2016 (see Exhibit 2). The Dow Jones Sukuk Higher Quality Investment Grade Select Total Return Index, which seeks to track sukuk from specified countries of risk, gained 3.54% for the period. The S&P MENA Sukuk Index, which is designed to measure sukuk issued in the Middle East and African market, advanced 3.97% in the same period.

Among the ratings-based subindices, the sukuk rated ‘BBB’ outperformed and rose 4.84% YTD, while the sukuk rated ‘AA’ also went up 4.43% in the same timeframe. The longer-maturity indices performed better than the shorter-maturity ones, reversing the trend in 2015. As of Nov.30, 2016, the Dow Jones Sukuk 5-7 Year Total Return Index and the Dow Jones Sukuk 7-10 Year Total Return Index gained 6.22% and 5.71% YTD, respectively.

Exhibit 2: Total Return Performance of the Dow Jones Sukuk Index Series

[1] Source: Thomson Reuters Eikon. Data as of Nov 8, 2016.

The posts on this blog are opinions, not advice. Please read our Disclaimers.