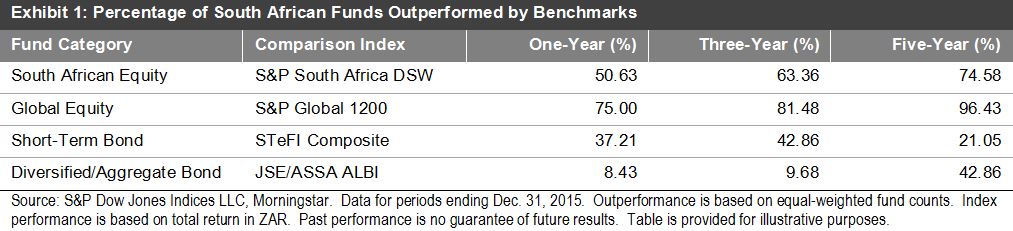

In 2015, equity markets in South Africa were turbulent amid falling commodity prices and the depreciation of the South African rand. Political uncertainty surrounding the appointment of the country’s finance minister and the lowering of the country’s debt rating by leading rating agencies also contributed to the lackluster performance of equities. This may partly explain why the S&P South Africa Domestic Shareholder Weighted (DSW) Index underperformed the S&P Global 1200 by 29% in rand terms.

Volatility in the markets would normally be favorable for active managers, who could make use of their stock-picking skills to benefit from the perceived discrepancies in the market. However, the SPIVA South Africa Year-End 2015 Scorecard shows that over 50% of active funds underperformed the domestic benchmark over a one-year period. The level of underperformance continued to deteriorate over the three- and five-year periods (see Exhibit 1). As for global equity funds, the performance of active funds against their benchmark was even more underwhelming, as 75% of active funds underperformed the benchmark over a one-year period. This rose to over 96% over the five-year period.