Monday’s stock market crash coming on the heels of the US market fall on Friday, August 22nd is creating jitters for investors around the world. However the signals have been around for some time, with many predicting for some time an end to the bull run that US market has enjoyed for the last 6 years leaving valuations at an all-time high and China’s own stock market run up of more than 150% in the last one year.

The devaluation of the Yuan was highly unexpected by market participants, and as a result, the market reaction was very strong and erratic. Many are once again calling China a “currency manipulator” and fears are rampant that this is a sign of major weakness in the Chinese economy as the authorities are desperate to prop up exports. In the end the devaluation appears to have sent a signal that the Chinese economy is weaker than understood and if the idea was to prop up exports or stocks markets, it has done the opposite. Due to its linkage to the dollar, the Yuan has strengthened substantially over the past year – in relation to most global currencies including many of China’s most important Asian export markets such as Korea, Taiwan and Thailand. This, along with domestic economic weakening, has created downward pressure on the Yuan relative to the dollar and the Chinese authorities have, in recent months, been actively propping up the currency to maintain stability versus the dollar. In this context, a 4% depreciation of the Yuan versus the dollar seems like a rather modest decline and the intervention may be better described as a minimal effort to stabilize exports as the Yuan remains relatively strong compared to other global currencies.

Chinese currency devaluation is also viewed by some as a desperate effort to shore up its declining stock market. China has the delicate task of managing a slowing economy, an exchange rate made vulnerable by this slowing growth, a depressed stock market and the temptation to keep exchange rates low. Whatever may be rationale for the currency devaluation, the world is extremely worried about a slowdown of the world’s second largest economy and the response has been seen in the global stock market meltdown starting in the US on August 22nd and continuing globally the following Monday.

Examining the direct impact of Chinese currency movements on the Indian economy and stock markets there are several strains immediately visible. A cheaper Yuan makes it even more difficult for Indian exports to compete with Chinese exports as in textiles and apparels. Slowing Chinese economy also means lower commodity prices globally which hurts Indian commodity producers though helps the overall inflation levels to come down. Though the S&P BSE SENSEX has remained relatively flat in the last three months, it succumbed to global fears over the weekend with the SENSEX down 8.5% accompanied by an accompanying sharp fall in the INR. The real impact can be witnessed in the USD version of the SENSEX. The S&P BSE Dollex 30 has fallen 11.9% in the wake of the RS.3 depreciation brought on by the stronger dollar. A weaker rupee reduces the amount FIIs reap on stock market returns giving them less reason to bring in inflows to the Indian market.

Global stock market volatility is expected to remain given the weak Chinese economy and the expectation of an interest rate rise in the US. India’s Reserve bank Governor has assured that they are well prepared to defend the rupee against a further fall with USD 354 billion chest and it is to be noted that the Rupee has not yet slid to its previous low of Rs. 68.80. Consumer price inflation is also under control at least in the immediate term though it remains to be seen if it can be sustained. No doubt falling commodity prices will help contain inflation.

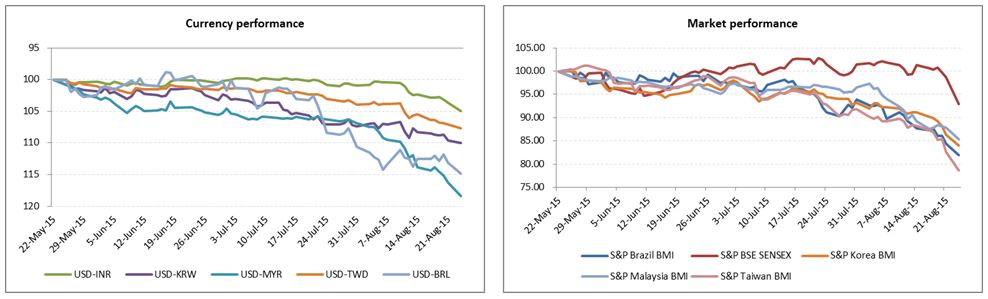

Comparing Indian stock markets to other major emerging markets, the picture is a lot rosier. Looking at chart 3, we see that the Indian Rupee has been holding up better against the US dollar and its stock market performance has also been more stable. The Indian authorities have rushed in to calm fears. While the short term may remain volatile given global fears, in the long term the stronger fundamentals should help the Indian market.

- India/China –

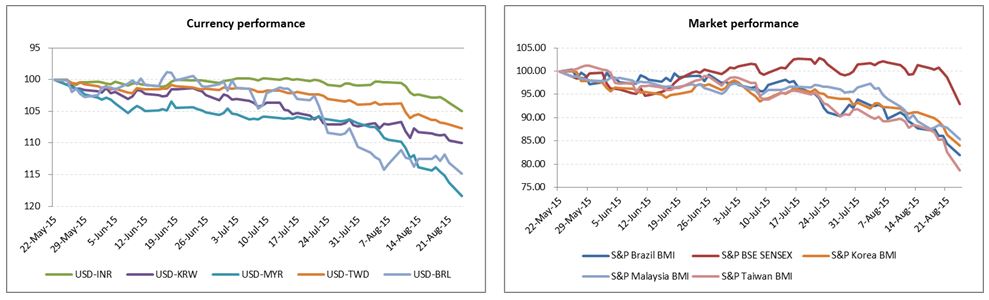

- Select Asian countries ex-China –

Source: Currency quote sourced from Bloomberg; total returns indices in local currency sourced from S&P Dow Jones Indices, from Dec 31, 2014 up to Aug 24, 2015.

| Currency code | INR | CNY | USD | KRW | MYR | TWD | BRL |

| Currency description | India Rupees | Chinese Yuan | United States Dollar | Korean Won | Malaysian Ringgit | Taiwan Dollar | Brazilian Real |