Malaysian ringgit continued the plunge and hit a 17-year low. The offshore holding of Malaysia local government debt also fell with the heightening FX volatility and declining FX reserves. The S&P Malaysia Bond Index dropped 1.27% in August, bringing year-to-date (YTD) total return to 1.66%. Its broader benchmark, S&P Pan Asia Bond Index, aggregates the returns from 10 countries in Pan Asia and calculated in USD, dropped -0.56% YTD.

Nevertheless, Malaysia has better fundamentals comparing with other Asian countries. Malaysia has been assigned solid credit ratings of A-/A3/A- . It also released better-than-expected 2Q15 real GDP growth at 4.9% y-o-y.

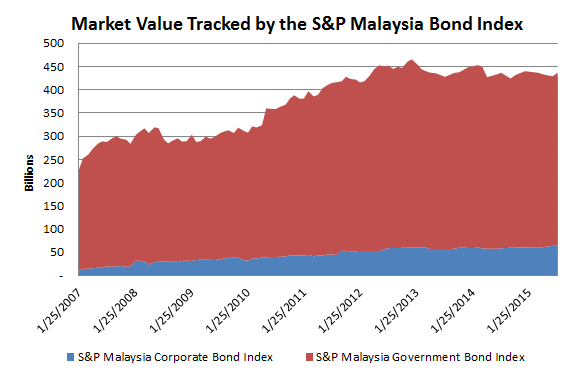

In fact, the Malaysian bond market almost doubled its size from 2007 to currently MYR 423 billion. Similar to other Asian bond markets, the corporate bond market expanded rapidly from a merely 5% to 15% of the overall market. Among the corporates, over 90% of exposure belongs to financials sector, with popular names like Malayan Bank, CIMB Bank, Public Bank and RHB Bank.

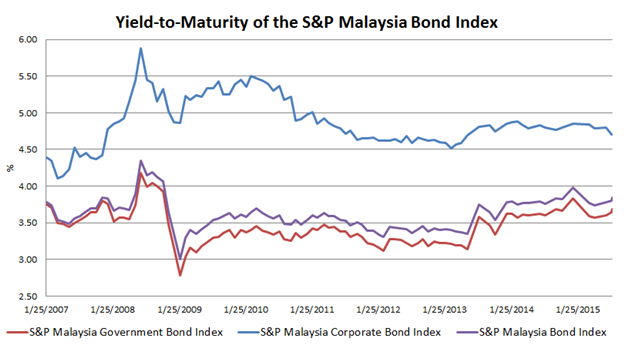

Looking at the yield performance, the yield-to-maturity tracked by the S&P Malaysia Bond Index has widened 17bps YTD to 4.14%, as of August 18, 2015. The yields of the S&P Malaysia Government Bond Index and S&P Malaysia Corporate Bond Index currently stand at 4.02% and 4.78%, respectively.

Exhibit 1: Market Value

Exhibit 2: Yield-to-Maturity

The posts on this blog are opinions, not advice. Please read our Disclaimers.