November Highlights:

- Islamic Indices Continue to Outperform Conventional Benchmarks Globally

- U.S. Markets Power Higher While Europe, Asia-Pacific and Emerging Markets Weaken

- MENA Equity Markets Sell off Sharply in October & November, Trimming 2014 Gains

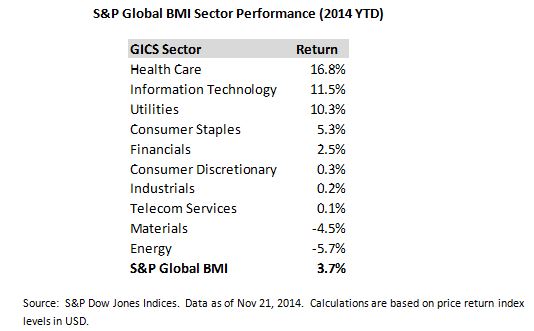

Most major Shariah-compliant benchmarks continue to outperform their conventional counterparts in 2014 as Information Technology and Health Care – which tend to be overweight in Islamic Indices – have been sector leaders, and Financials – which are underrepresented in Islamic indices – have experienced some weakness. One notable exception has been in the Middle-East where equity markets have very little exposure to Information Technology and Health Care and thus Shariah-compliant indices have not benefited from the strength in these sectors.

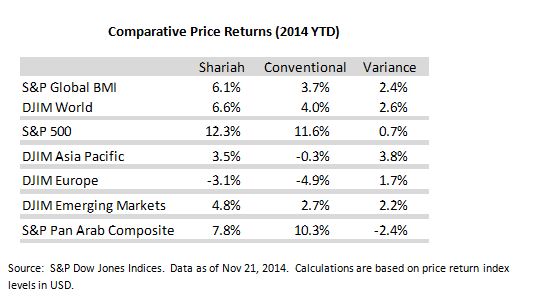

As of November 21, 2014, the Dow Jones Islamic Market World and S&P Global BMI Shariah Indices gained 6.6% and 6.1%, respectively, for the year, each outperforming their conventional counterparts by about 250 basis points. However, performance has been highly divergent across regions with the U.S up double-digits, while European regional indices are in the red. The Dow Jones Islamic Market Asia Pacific had been outperforming the U.S. and other developed market regions through late August. However, Asian markets have cooled in the past 3 months, while the S&P 500 Shariah has reached new highs following a short-lived bout of volatility in October. Outside of MENA, where the S&P Pan Arab Composite Shariah has underperformed the conventional S&P Pan Arab Composite, all other major regional Shariah-compliant indices remain ahead of their conventional counterparts through November 21.

MENA equity markets have cooled markedly following substantial gains earlier in the year. After peaking on September 8, up nearly 26% for the year, the S&P Pan Arab Composite Shariah declined 14.3% through November 21, leaving its year-to-date gain at a more tepid 7.8%. Weakness was experienced across the region, although Saudi Arabia was a major driver of the negative performance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.