Over the course of last week, yields on all on-the-run bonds moved lower. The yield on the S&P/BGCantor Current 10 Year U.S. Treasury Index closed Friday 11 basis points lower at a 2.67%. During the week the Treasury did auction $32 billion 2’s, $35 billion 5’s and $29 billion 7-year notes. Though the 2-year auction was considered weak, flight-to-quality trades and overseas interest helped the 5 and 7 year auctions along.

This morning the focus has been on this week’s Federal Reserve meetings and the Ukraine crisis as the U.S. issued sanctions targeted seven individuals and seventeen Russian companies. At the same time the European governments have named 15 individuals to the list. In addition to political news, March U.S. Home Sales month-over-month was stronger than expected reporting 3.4% as only 1% was expected. In addition to Home Sales, the Dallas Fed Manufacturing Outlook also reported a stronger 11.7 versus the expected 6.0. The rest of the week is full of potential market moving triggers as the S&P/Case-Shiller Home Price Index along with Mortgage Applications, the ADP Employment Change (210k expected), 1st quarter GDP Price (1.6% exp.) and the FOMC Rate Decision are slated for tomorrow.

The FOMC Rate Decision being the highest priority of the bunch. Tapering and other main policy targets of the Fed are expected to remain unchanged. Beyond Wednesday of this week, Initial Jobless Claims (320k exp.), ISM Manufacturing (54.3 exp.), Nonfarm Payrolls (215k exp.) and Unemployment (6.6% exp.) potentially will shed more insight into the degree of strength to the economy.

This week the Treasury will auction $15 billion of a 2-year floating rate note maturing in 2016. This is a new addition to the already existing $41 billion Jan. 31, 2016 floating rate notes which are returning 0.02% month-to-date as measured by the S&P Current 2-Year U.S. Floating Rate Treasury Index.

On the month and the year, investment grade corporate bonds are outperforming high yield. The S&P U.S. Issued Investment Grade Corporate Bond Index has returned 1.06% month-to-date and 4.0% year-to-date. While in comparison the S&P U.S. Issued High Yield Corporate Bond Index has only returned 0.5% and 3.48% respectively. The OAS (Option Adjusted Spread) of the investment grade corporate rating sub-indices are tighter: AAA (-6 bps), AA (-2 bps), A (-3 bps) and BBB (-5 bps) while high yield’s BB and B are flat and the CCC & below are 22 bps wider.

The S&P/LSTA U.S. Leveraged Loan 100 Index still remains lackluster as the index is down -0.06% month-to-date and is only returning 0.94% year-to-date. The index’s yield has risen 17 basis points since the beginning of the month and is presently at 5.62%. The weekly review of this index gives it a floating rate quality.

Source: S&P Dow Jones Indices, Data as of 4/25/2014, Leveraged Loan data as of 4/27/2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

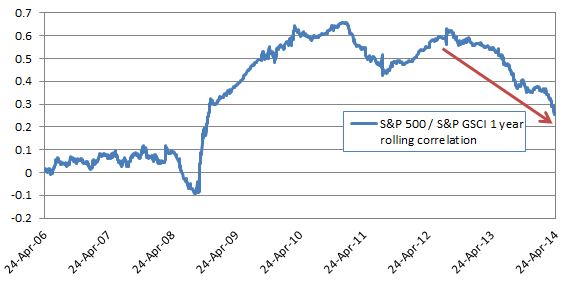

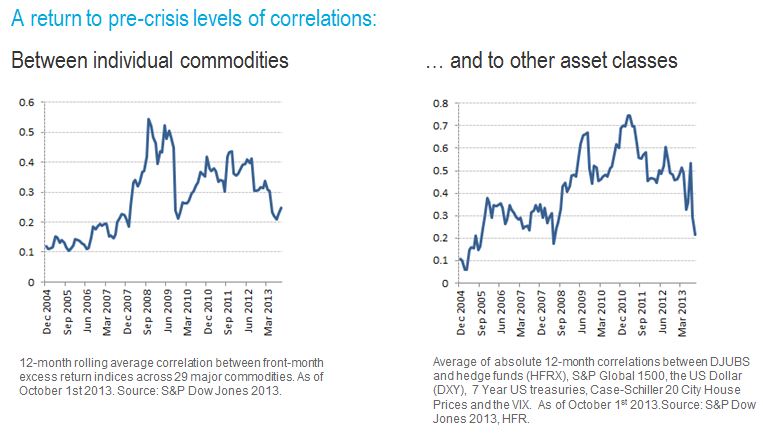

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and

Notice in the charts above that both correlation of commodities to each other and to other asset classes has fallen to precrisis levels of about 0.2, indicating little movement together with stocks and bonds and little movement together with each other. This makes commodities, once again, an asset class to provide diversification, and