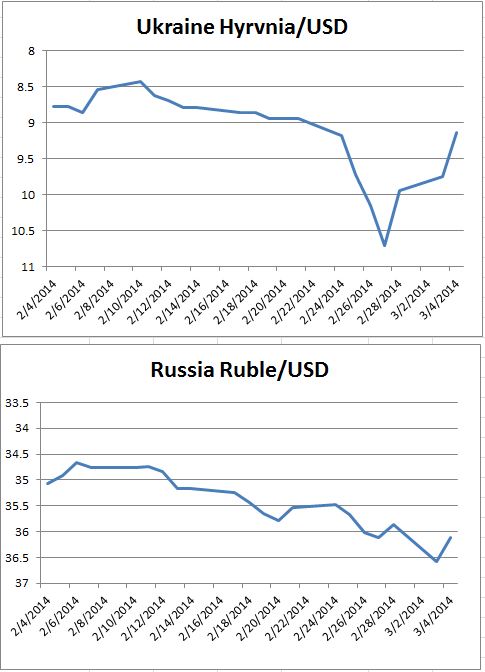

Central Banks persist in fighting inflation. The Fed is tapering and talking about tighter money. The European Central Bank won’t cut interest rates. Only in Japan, where the Prime Minister is pushing the Bank of Japan is there a hint of a different approach.

Inflation rates in most developed markets are below central bank targets of 2%. In the US the Personal Consumption Expenditures deflator – the Fed’s preferred measure – puts inflation at 0.9% over the four quarters of 2013. The Eurozone consumer price index is a touch lower at 0.8% for the year ended in February. Japan is the surprise leader with consumer prices up 1.1% after spending 2-1/2 years in negative territory. All this raises two questions: what is so bad about deflation and why aren’t central banks doing something?

Deflation is falling prices – not just gasoline at $4 a gallon or the cost of health insurance – almost every price falls. Deflation leads to stagnant economies and depression. The problem is the prices that don’t fall. In most economies wages and salaries rarely adjust downward. Whether by convention, union contracts or competition for workers, wages are sticky. As prices fall, employers face rising real (inflation adjusted) labor costs. One reason why job growth is still weak five years after the recession and many new jobs offer very low wages is that with inflation almost zero, the relative cost of labor is higher than it used to be. The second problem is debt. With deflation the real value of debt rises, paying off debt becomes harder and defaults multiply. The housing crisis was a limited example – home prices fell, incomes were stagnant and mortgage defaults rose. When the amount of money and credit in the economy collapse, prices and economic activity collapse. That was the fall of 2008. Despite the Fed’s timely response to pump money and credit into the economy, we are still on the edge of deflation today.

Central banks could be more aggressive about deflation, but are more concerned with far distant future inflation. Economic policy is, hopefully, based on good economic analysis; it is also based on primal fears and (re)fighting the last war. The first hand history of monetary policy in the US that economists and bankers can personally recall goes like this: 1970s saw rampant double digit inflation, Paul Volcker saved the economy and the Fed by ending inflation with a deep recession, setting the stage for two decades of economic growth and all was fine until home price inflation spooked the Fed and led to the financial crisis. The last war was the end of inflation in 1979-82. Forgetting that lesson would a terrible thing.

In Europe the primal fear is Germany’s hyperinflation in the 1920s lead to Depression and the Second World War. For sixty years Europe was committed to preventing another inflation – either successfully in Germany or with frustration in other countries. This is why the Bundesbank, Germany’s pre-euro central bank, is held up as the model for the current European Central Bank.

Muddling along on the edge of deflation leaves the economy with more risk of collapse and too little growth. The answer is not for the Fed to stop tapering and introduce QE4. A better approach is fiscal policy – both spending and tax reform. The economy can afford some fiscal stimulus, especially to rebuild basic infrastructure like roads, bridges and airports.

The posts on this blog are opinions, not advice. Please read our Disclaimers.