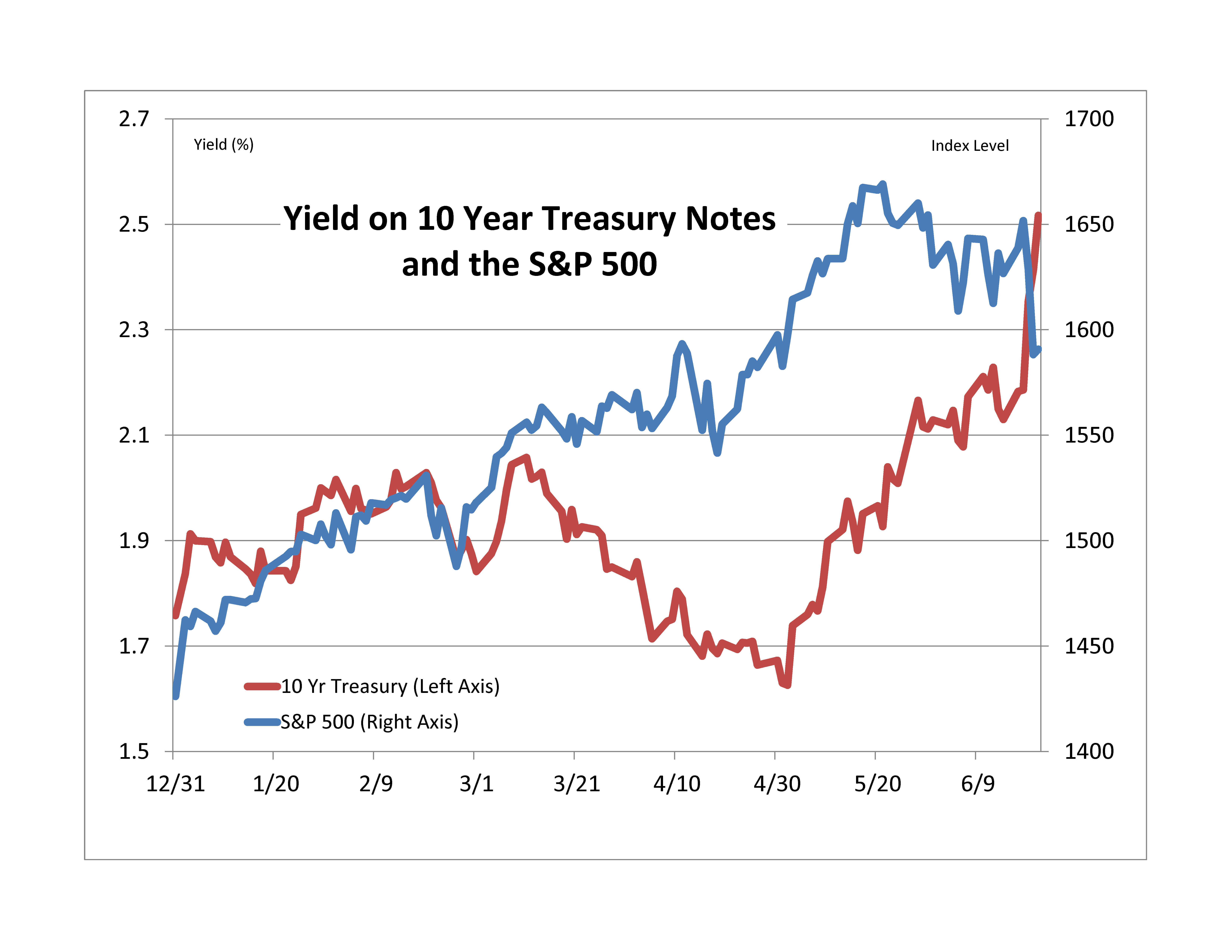

Since roughly the beginning of May, U.S. interest rates have been in an uptrend, with the 10 year Treasury note ending last week at a yield of 2.5%. Equity markets, not surprisingly, have reacted by weakening, especially in last week’s trading.

Some of us of a certain age will admit to a degree of bewilderment at this, since a 2.5% 10 year rate would have seemed ridiculously, if not unattainably, low for the vast majority of our working lives. Why are markets reacting so negatively to what, in most historical contexts, would have been considered a very favorable rate environment?

The answer lies in the distinction between high rates and rising rates. A 2.5% Treasury yield is unquestionably not high by any reasonable historical standard, but rates have equally unquestionably been rising for the last two months. When rates are stable, whether high or low, the equity market is priced to reflect their stability. When rates change, the equity market adjusts to reflect the change. As with many other phenomena in economics, it’s not the level of a variable that makes the difference, but the variable’s rate of change.

Stable rates, other things equal, enhance the stability of equity returns. Rising rates, if indeed they do continue to rise, may present a continuing challenge.

The posts on this blog are opinions, not advice. Please read our Disclaimers.